How Direct Debit works in Australia: Your expert guide for 2025

In Australia's rapidly digitising economy, securing reliable cash flow and fostering customer loyalty are more critical than ever for business success. While new payment technologies emerge, one method has remained a cornerstone of the nation's financial infrastructure due to its unmatched reliability for recurring payments: Direct Debit. This guide provides an expert, up-to-date overview of how direct debit works in 2025, its strategic benefits for your business, and its place in the future of Australian payments – including how it solves the common and costly payment challenges faced by Australian Small and Medium Businesses (SMBs).

Payment challenges facing Australian SMBs in 2025

Running a business means handling many responsibilities, but payment processing shouldn’t take up a disproportionate time or hinder cash flow. Unfortunately, many SMBs face significant payment friction, costing time, money, and customers. According to our 2025 SMB Payments research:

- Australian SMBs lose an average of 22.6 hours per week managing payment administration tasks like reconciliation and chasing late payments.

- 1 in 6 payments arrive late, delaying cash flow and creating unpredictability.

- 1 in 4 SMBs say payment friction has caused them to lose customers.

- Most SMBs juggle approximately 3.5 different payment methods across multiple providers, increasing complexity and admin effort.

- Despite this, 93% of SMBs are open to consolidating payment providers, but only 20% have made that change.

In this guide we’ll cover:

-

How Direct Debit works in 2025

-

Direct Debit in the 2025 digital economy

-

What is Direct Debit?

-

Why would I use Direct Debit?

-

How do I use Direct Debit?

-

Is Direct Debit safe?

-

What are the benefits of Direct Debit for my business?

-

How do I set up a Direct Debit?

-

How do I cancel or change a Direct Debit?

-

How often are Direct Debit payments made?

-

Are my customers under contract using Direct Debit?

-

Do I need to invest in expensive software to offer Direct Debit?

-

How does Direct Debit compare to other payment methods?

-

How to get set-up Direct Debits with Ezidebit Australia

The enduring power of Direct Debit in Australia's 2025 digital economy

The scale of direct debit usage in Australia underscores its fundamental importance to the national economy. The system's relevance has not diminished in the digital age; it has magnified. In 2024, the Bulk Electronic Clearing System (BECS) - the framework that facilitates direct debit - processed a staggering 3.5 billion payments with a total value of $17.4 trillion. This figure, provided by the Reserve Bank of Australia (RBA), represents nearly 90% of the value of all retail account-to-account payments in the country, highlighting its role as the primary system for a vast range of critical transactions, including salaries, welfare, subscriptions, and regular bill payments.

This enormous volume and value demonstrate that as Australia's economy has grown and moved away from physical cash, direct debit has remained the trusted, foundational infrastructure for high-volume, automated payments. The trend away from cash is stark: in 2007, cash was used for 70% of in-person payments, a figure that plummeted to just 16% by the end of 2022. Direct debit is an integral part of this digital shift, providing the stability and efficiency that both businesses and consumers demand. For a business owner, choosing to implement direct debit means leveraging a proven, robust, and economically vital system.

What is Direct Debit?

At its core, direct debit is a simple concept: it is an instruction a customer gives to a business, authorising them to collect money from their bank account or credit card on an agreed-upon schedule. This authorisation is the cornerstone of the entire process and is formalised through a Direct Debit Request (DDR). Once the DDR is in place, the business can automatically "pull" the authorised funds for recurring payments, making it a popular and highly effective method for any business with ongoing billing cycles.

Direct debit payments from a bank account in Australia are processed through the Bulk Electronic Clearing System (BECS). Managed by the Australian Payments Network (AusPayNet), BECS is a highly reliable batch-processing system that has been the workhorse of the Australian economy for over 30 years, handling bulk electronic transactions by grouping them together and exchanging them between financial institutions at set times throughout the day.

Every BECS direct debit payment is listed on the customers’ bank account in two fields including: the name of the merchant (business) and the lodgement reference unique to the transaction. These are known as statement descriptors.

For example, the following statement descriptors apply to customers of businesses who use Ezidebit in Australia:

-

For bank accounts, your business name (first 16 characters) will display on the account holder’s statement.

-

For credit cards, the descriptor will be EZI* <business> (first 16 characters).

For businesses that use Ezidebit in New Zealand, Merchant Identification Names (MID) are displayed on the statement. MID names display Ezidebit’s name and a reference to the industry of the business you have a direct debit agreement with. For example, EZIDEBIT HEALTHFIT, EZIDEBIT STORAGE or EZIDEBIT ACCOUNTING.

Why would I use Direct Debit?

Direct debit doesn't require card numbers, PINs, passwords or any other sensitive data, making it a highly secure and reliable payment solution.

When considering a direct debit payment provider, make sure you choose one that is Level 1 fully compliant with the Payment Card Industry Data Security Standard (PCI-DSS).

Modern cybersecurity threats are becoming more sophisticated and it’s understandable that many businesses are concerned about the security and safety of their payment processing options.

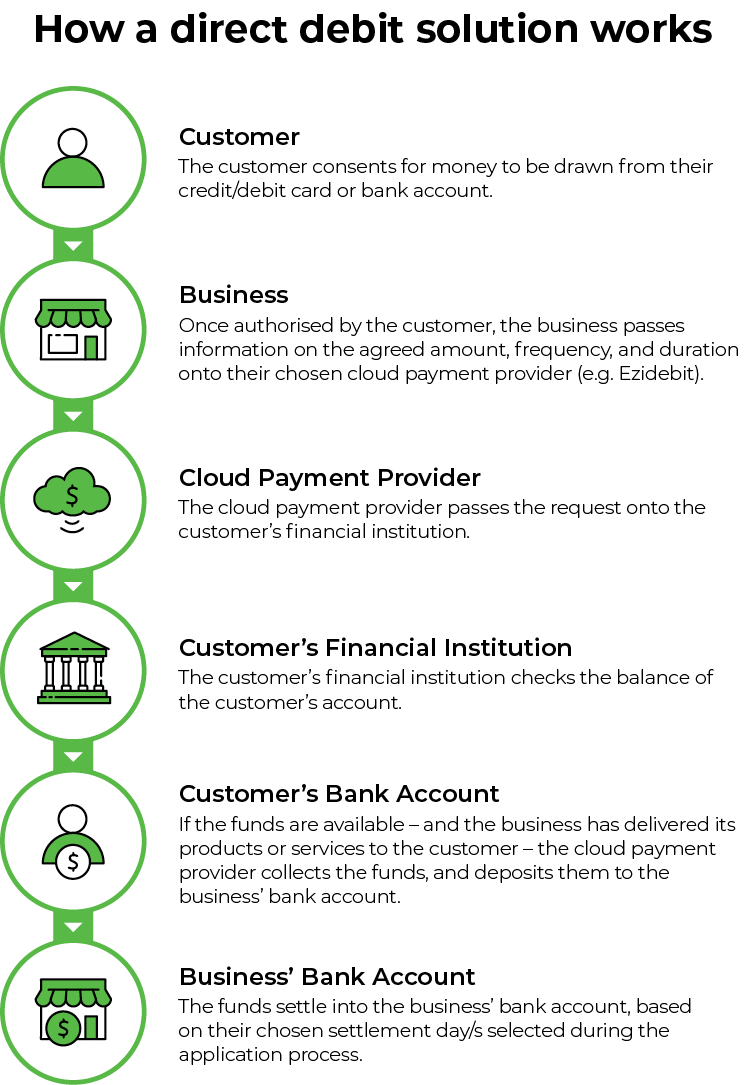

How does Direct Debit work?

Direct debit is an easy way for a customer to pay a business for a recurring service or product. A business and its customer come to a signed agreement for an agreed amount, frequency and duration. Once authorised by the customer, the business’ chosen payment provider (e.g. Ezidebit) will collect the agreed funds and deposit them into the business’ account.

This authorisation from the customer ignites a chain of communication between the business, cloud payment provider, and the customers financial institution as illustrated below.

What are the benefits of direct debit for your business?

-

Secure payment method: Direct debit is a highly secure and reliable payment method, particularly when you use a payment provider that is fully PCI-DSS compliant.

-

Easy to set up, easy to run: Modern paperless solutions are extremely streamlined and automated, with customers able to quickly and easily authorise the service. Once authorised, customer payments are handled automatically with very little input from the customer or the business.

-

Constant, reliable cash flow: Improve the speed and amount of your inbound cash flow, to give you a more accurate forecast of incoming revenue and outgoing expenses.

-

Less awkward money chat: It’s time to stop having awkward conversations with your customers about late payments or unpaid accounts. Don’t rely on your customers to remember to pay their monthly invoice or fortnightly payment. Instead, you can receive funds on a set schedule that works for both you and your customers.

-

Plenty of flexibility: Just because it’s recurring, a good direct debit payment solution isn’t rigid or inflexible. Your solution should cater for adjustments of payment terms throughout the life of the contract; for example, allowing you to easily tweak payment schedules to suit your customers’ personal commitments such as taking an extended holiday or travelling for work.

-

Encourage customer retention: Direct debit is a great way to encourage customer retention and improve recurring revenue. This is because it creates a simple payment method that can easily be renewed and maintained over long periods of time. Your customers don’t have to continuously set up payments to your business, it happens automatically.

-

It’s not expensive to implement: A direct debit solution tailored to the needs of your business can be extremely affordable and easy to integrate. Plus, it should be cloud-based, so there’s no hardware required to be purchased.

How do you set up a Direct Debit?

Setting up direct debit payments for your customers is easy. Today, paperless direct debit solutions are extremely streamlined and automated to make it a simple set-up process.

You can offer your customers multiple methods to set up direct debit, including:

Online form: You can share a form via a link or hyperlink a button on your website. Customers will need to fill out their details and authorise the agreement. Once completed, the payment schedule will become active.

Email payment request: You can trigger a notification request from your payment platform directly to your customer to complete a digital direct debit request agreement. Once they enter their payment details and authorise the agreement, the payment schedule will become active.

In person: If your customer is with you, simply enter their details straight into your payment provider’s system or via integrated software. They can enter their payment details and authorise the plan on the spot for instant approval.

Paper form: Your customers can fill in and sign a hard copy of a Direct Debit Request (DDR) form. You’ll then need to enter their details into your payment provider’s portal or your integrated software. The signed DDR form must be stored securely by your business, in accordance with PCI-DSS requirements.

How do I cancel or change a Direct Debit?

Your customers simply contact you if they wish to amend, pause or cancel their payment schedule. You can update this yourself either directly through your payment provider’s portal or integrated business software.

But keep in mind that while most changes can be made online, there may be some adjustments that require a new direct debit form to be completed. This is required when the goods or services being delivered change from the original agreement.

Some scenarios where a new direct debit agreement needs to be made include:

-

A fortnightly gym membership being moved to a monthly debit on a new amount with a renewed 12 month agreement.

-

A customer has been paying for service A (i.e personal training) and now wants to combine service A and service B (i.e personal training and nutrition plan).

In the examples mentioned above, rather than an adjustment to the days that are being billed (which can be done online without a new agreement), the services offered for the payment have changed completely.

How often are Direct Debit payments made?

This is up to you as the business owner, and can be tailored to suit your requirements.

You could:

-

Align it with your business expenses: For example, if you pay business’ rent, staff and utilities monthly, your customer payments can be put on the same schedule or more frequently.

-

Charge less, more frequently: By breaking down larger payments into small-bite sized amounts, you can help your customers manage their cash flow. This will also decrease the likelihood of late or dishonoured payments.

Are your customers under contract using direct debit?

Direct debit is a mutual agreement, not a contract. While it offers your customers a more manageable way to pay, there is no legal commitment.

However, it's common for businesses to ask their customers to sign a separate agreement with their own specific terms and conditions, such as a 12-month gym contract. This particular agreement is binding, but the direct debit is a separate agreement outlining the payment method, and is not a guarantee or legal contract of funds.

Your customers should feel encouraged and liberated by the flexibility of a payment method, not trapped by it, which will help gain their loyalty and trust. With direct debit, this is easy to achieve.

Do I need to invest in expensive software to offer Direct Debit?

No. Using a cloud-based direct debit solution is simple to set up and quick to transition your customers onto.

How does Direct Debit compare to other payment methods?

Some companies rely on just one payment method such as direct debit. Others need a combination of direct debit and other payment methods to ensure they are providing their customers with the best payment experience possible.

Our research shows that SMBs juggle an average of 3.5 payment methods across multiple providers, which increases complexity and admin load. Direct Debit can help streamline recurring payments into a single automated process, reducing the need for manual handling across platforms.

What are the main differences between direct debit and other payment methods?

|

Payment Method |

Best for |

Top benefits |

|

Direct Debit |

Recurring or regular transactions |

|

|

Real Time Payments |

Instant payments |

|

|

BPAY |

Larger or one-off transactions |

|

|

EFTPOS |

Card-present transactions |

|

There’s no doubt the payments landscape is continually changing and it has never been more important to offer seamlessly integrated payment technology.

Ezidebit’s payment product suite helps you bring Direct Debit, EFTPOS, BPAY and Real Time payments together for simplicity and ease.

Every payment and the customer data that comes with it is handled and processed securely within Ezidebit's level 1 PCI-DSS compliant system.

Our flexible solution allows you to have complete control and visibility, ensuring you can continue to deliver greater value and a better payments experience than your competitors!

Get in touch with one of Australia's leading Direct Debit Providers today

Click here to get in touch with us and we’ll customise a solution for you to suit your business’ needs. Then you simply need to fill in an application form, and we’ll work with you to get your account established and ready to use. Direct debit with Ezidebit, the only set-and-forget payment system you’ll need.