Unified payments, real outcomes for ISVs

8mins

When payments are unified, the business model changes – not just the provider

Most conversations about unifying payments start with technology. APIs, integrations, migration effort, and risk mitigation tend to dominate early thinking.

But for ISVs, the biggest shift isn’t technical. It’s operational.

Unified payments are not the same as omnichannel payments. Omnichannel focuses on supporting multiple channels — online, recurring, and in‑person. Unified payments go deeper, aligning those channels behind a single operating model with shared ownership, consistent flows, and a common foundation.

In practice, unified payments rarely mean using a single gateway for everything. Not all vendors offer the same breadth of channel support, and it’s likely no one gateway will cover every use case a merchant may want. The goal for most ISVs is intentional consolidation: anchoring as much as possible to a primary payment gateway, and adding others only where genuine capability gaps exist.

Done deliberately, this approach limits fragmentation, preserves cohesion across payment instruments, and enables more consistent experiences for payers as they move between channels. When payments are unified in this way, platforms change how they deliver value — how trust is established, how adoption compounds, how revenue behaves, and how quickly teams can move. Those outcomes matter far more than the act of switching itself.

Why unified payments is an operating-model decision

In fragmented payment environments, teams work around complexity. Product ships with constraints. Support manages exceptions. Finance reconciles across systems. CX absorbs the inconsistency.

Unification simplifies that operating model.

Instead of aligning multiple providers, rulesets, and reporting views, teams operate from a shared foundation. One flow. One owner. One source of truth.

That shift creates outcomes you can observe and measure — well before any full consolidation story is told.

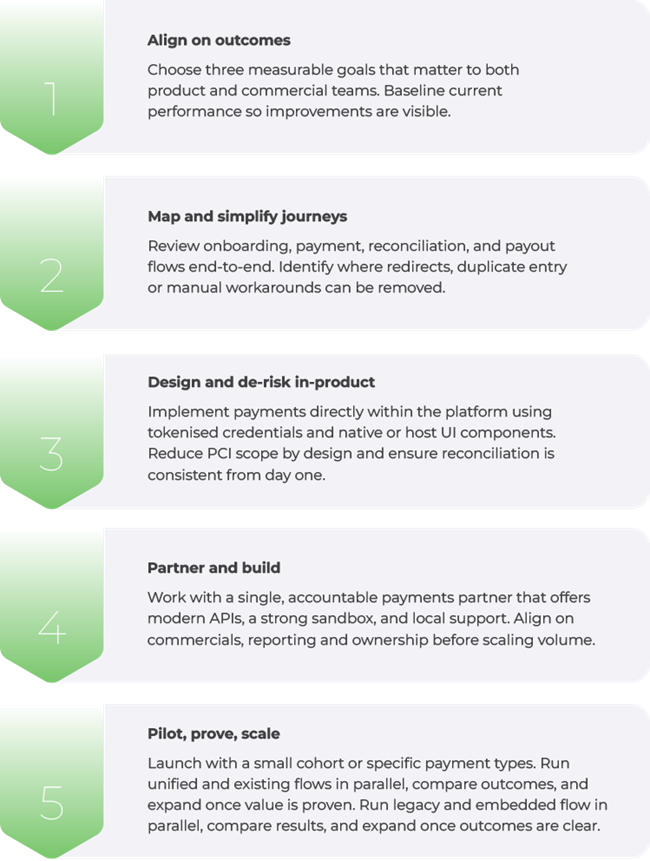

The above diagram illustrates a five-step framework ISVs can use to move toward unified payments, from aligning on outcomes to piloting and scaling improvements.

Five outcome dimensions that change with unified payments

1) Trust and risk management

Unified flows reduce ambiguity. Ownership is clearer. Exposure points are fewer. Resolution paths are easier to explain — internally and to customers.

What to measure:

- Time to resolve payment‑related support and dispute issues.

- Volume of escalations requiring third‑party hand‑offs.

- Consistency of audit and reporting outputs across channels.

When trust improves, it tends to show up quietly through fewer edge cases and faster confidence in next steps.

2) Embedded stickiness

When payments live naturally inside the platform, they become part of everyday workflows. Subscriptions, invoicing, refunds, reconciliation, and reporting happen where users already operate.

What to measure:

- Adoption of embedded payment features over time.

- Retention and churn differences between merchants using embedded payments and those who are not.

- Reduction in “where is my payment?” and admin‑driven support tickets.

Stickiness compounds when payments feel like part of the product, not an external dependency.

3) Differentiation through consistent experience

Consistency matters. Customers notice when checkout, authentication, and post‑payment steps behave the same way across channels and use cases.

What to measure:

- Drop‑offs and retries in payment flows.

- Volume and nature of CX‑related complaints tied to payments.

- Reduction in bespoke or one‑off payment configurations requested during sales cycles.

Unified payments support differentiation by making experience predictable, not flashy.

4) Predictable revenue and clearer economics

Fragmentation often obscures economics. Fees, revenue shares, and support costs are spread across systems and teams.

Unification brings clarity.

What to measure:

- Attach rate of payments across your merchant base.

- Revenue per account where payments are embedded.

- Cost‑to‑serve indicators linked to payment support and reconciliation effort.

Clearer economics make commercial decisions easier, and scaling more deliberate.

5) Faster innovation through a single foundation

With one integration and one roadmap, teams spend less time maintaining parity and more time improving outcomes. With a single, PCI‑compliant integration, teams can focus less on maintaining parity across systems and more on improving outcomes that matter.

What to measure:

- Lead time for payment‑related releases.

- Number of systems touched per change.

- Regression and defect rates linked to payment functionality.

Speed improves not because teams rush, but because friction has been removed.

How to evidence progress without over‑committing

Unified payments don’t need to be proven all at once.

Start with:

- A small, representative merchant cohort.

- Baseline metrics across the five outcome areas.

- A clearly defined pilot with shared success criteria across product, commercial, and support.

This approach makes outcomes visible early, without asking teams to take on unnecessary disruption.

Closing thought: outcomes matter more than architecture

Unified payments are not valuable because they are unified. They are valuable because they change how platforms operate — how teams work, how customers feel, and how growth compounds.

For ISVs, the real question is not “can we unify?”, but “which outcomes matter most — and how will we measure them first?”

Key takeaways

- Unified payments change operating models, not just technical setups.

- Trust, adoption, differentiation, revenue clarity, and speed are observable outcomes.

- Measuring outcomes early reduces perceived migration risk.

- Pilots and baselines make progress visible without committing to a full overhaul.

If you had to prove the value of unified payments six months from now, which outcome would you measure first?

Download the ISV Payments CX Playbook to explore the five outcome dimensions in more detail and map a low‑risk path forward.